Belrise Industries Limited (BIL), one of India’s leading integrated automotive component manufacturers with a diverse portfolio of safety-critical systems and engineering solutions announced its unaudited Financial Results for the quarter ended 30th June 2025

Consolidated Financial Highlights

Other Business & Financial Highlights (Q1 FY26)

- Manufacturing Revenue up 29% to ₹ 18,323 Mn. as compared to ₹ 14,247 Mn. in Q1 FY25

- Manufacturing Revenue as a % of Total Revenue stood at 81%

- Manufacturing EBITDA up 17% to ₹ 2,536 Mn. as compared to ₹ 2,160 Mn. in Q1 FY25

- Manufacturing EBITDA Margins stood at 13.8%

- Exports contributed 5.4% to our manufacturing revenue

- 72.7% of manufacturing revenue is from powertrain-neutral products

- RoACE stood at 14.4%

- IPO Proceed: Through the IPO proceeds, the Company has repaid debt to the tune of ~₹15,960 million leading to a reduction in Net Debt/Equity from 0.98x in Q1 FY25 to 0.16 in Q1 FY26

- Net Debt as of 30th June 2025 stood at Rs. 7,698 million after paying off debt to the tune of Rs. 15,960 million from the IPO proceeds

New Plant at Chennai: Commenced supplies from the newly inaugurated Chennai plant, which caters to two key customers — a leading premium two-wheeler OEM and a leading commercial vehicle OEM. The Chennai plant is expected to continue scaling over the next 2–3 quarters. The Company is also in discussions with a couple of other OEMs for nominations and new product supplies.

Key Operational Highlights for Q1FY26 2-Wheelers

- Successfully ramped up Chennai plant for a premium 2W OEM and leading CV OEM

Belrise Industries Limited

(Formerly known as Badve Engineering Limited)

- Commenced pilot production of two proprietary lines: Steering Column for a leading European OEM and Combination Braking System (CBS) for a Top-4 e-2W OEM

- Signed GPA with a Top-4 e-2W OEM

4-Wheelers

- Initiated integration of H-One India’s operations and development for an upcoming chassis program for a Japanese 4W OEM

Commercial Vehicles

- Marked BEL’s maiden entry into the M&HCV (Medium & Heavy Commercial Vehicle) segment with receipt of POs for Chassis parts from a leading CV OEM, thus increasing content per vehicle by INR 23,000

Others

- Marked BEL’s maiden entry into an Indian and an Israeli defense OEM; won incremental orders from another Indian defense OEM

Commenting on the Q1 FY26 performance, Mr. Shrikant Badve, Managing Director of Belrise Industries Limited said,

“Q1 FY26 marked a strong start to the year for Belrise Industries, building on the momentum from our listing and further strengthening our position as one of India’s leading integrated automotive component suppliers. The quarter also saw continued progress on strategic priorities, operational expansion, and portfolio diversification.

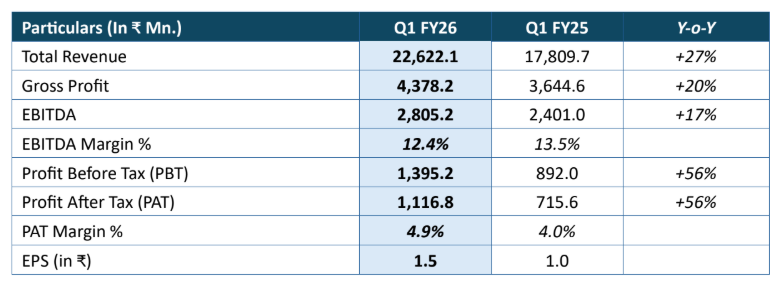

Total revenue from operations were ₹22,622 million, up 27% year-on-year, including manufacturing revenue of ₹18,323 million which grew 29% year-on-year, supported by increasing content per vehicle, higher order rollouts from our proprietary product portfolio, commercialization of the new Chennai facility and successful integration of H-One India into our basket of offerings. Our EBITDA stood at ₹2,805 million with margins at 12.4%.

A significant highlight this quarter was the commissioning of our new facility in Chennai, which is now commercially supplying a marquee two-wheeler OEM and a marquee commercial vehicle OEM as a single-source supplier across multiple components. This adds to our ongoing capacity expansion initiative, with new plants in Pune and Bhiwadi on track to ramp up operations in the coming quarters.

Our strategic transition from a Tier-1 component supplier to a Tier-0.5 system supplier continues to gain traction.

The acquisitions of H-One India and the plastic components business of Mag Filters are now being integrated into our operations. These bring specialized capabilities in high-tensile steel fabrication and proprietary filtration technology, enabling lightweighting and greater relevance across PV, CV, and 2W segments.

Looking ahead, the Indian auto component industry is expected to grow at a steady pace in FY26, led by the 2W and PV segments. With our expanded manufacturing footprint, diversified portfolio, and strong OEM relationships, Belrise is well placed to outpace industry growth and deliver favorable growth over the years. Our focus remains on penetrating further into our core 2W portfolio, scaling the 4W and CV segments, deepening OEM partnerships, driving proprietary product growth, and maintaining financial discipline.”