Organised as part of ACMA-Automechanika New Delhi from Feb 1-3 in Delhi, the conference brought together the entire value chain of the Indian aftermarket to address developments that are dramatically reshaping the industry.

The theme of the conference was ‘Indian Automotive aftermarket at an Inflection Point: How does it scale up amid opportunity and also an increasingly complex ecosystem?’

It opened with an inspiring address by Shraddha Marwah Suri, President, Automotive ComponentsManufacturers Association who emphasised the tremendous upside for the Indian aftermarket. Her thoughts were amplified by a white paper presented by TechSci Research.

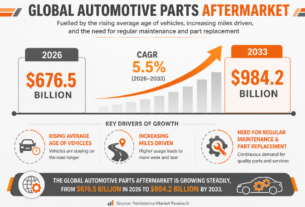

The white paper projected the Indian aftermarket to reach a level of USD 14.7 billion by FY 29 from the 2019 level of USD 10.1 billion. The market drivers we increasing levels of vehicle ownership and extended vehicle lifespan, greater demand for customization and personalization, alongside government initiatives to promote road safety. The challenges are spurious parts, automotive industry supply chain disruptions and the shifting momentum towards e-mobility which entails fewer moving parts and therefore reduced volumes.

The conference provided the opportunity to host a couple of panel discussions. Digitisation a boon or bane?

The first panel consisted of Rakesh Kher, CEO, Aftermarket vertical, Uno Minda; Sharad Bhatia, Head, MAHLE Aftermarket India & Head of MAHLE Service Solutions Asia Pacific; Oleksandr Danylenko, Founder and MD, Boodmo.com; Ravish Deshpande, MD, India and South Asia, TecAlliance; and K. Balasubramaniyam, Wholetime Director, Speed-A-Way. The discussion was moderated by Sridhar Chari, Consultant, MOTORINDIA.

Uno Minda’s Kher expressed, ‘digitisation is surely a boon. We already have more than a billion cellphones in use and many more devices enabled on Internet of Things. So, the trend towards online presence and transactions has only accelerated post the pandemic. Apps now help us track purchases for our own products and also competitive offers. Social media drives effective communication, while digital marketing helps uncover critical data. Artificial intelligence and machine learning tools optimise demand forecasting. Simultaneously digital tools are helping to streamline our supply chain, warehousing management and distribution channels. Today, some of our products are sold on e-commerce platforms.

People can shop online and buy offline or vice-versa. Consequently, some rungs in our distributionchannel are being dynamically realigned. Considering that we have 25-30 product lines and thousands of Stock Keeping Units, even a 4-5% improvement in the availability of the right inventory through digitisation will make a huge difference.’

Mahle India’s Bhatia complemented Kher’s thought process. ‘The aftermarket is seeded from the point of manufacture of a vehicle and its components, through 3D drawings. The sale of a vehicle triggers part sales and services under warranties. So, through smart packaging and digital tools, we keep track of the vehicle and component’s journey across applications and geographies. That way, we can be immediately responsive in the event of breakdown or failure. This mechanism helps inventory management and effective pricing. With the industry’s concerted effort, we see a significant reduction in the incidence of spurious parts. Such proactive monitoring of the full value chain is essential in the fragmented Indian aftermarket, where most customers prefer ‘do it for me’ rather than ‘do it yourself’.

The fragmented nature of the Indian aftermarket’s value chain was driven home by Boodmo.com’s Danylenko. ‘I moved to India nine years ago after successfully starting digital ventures in Ukraine. India surely has an exciting aftermarket and we were determined to make a quick and dramatic impact. But it has taken us a long while to understand the market. We may have an extremely user-friendly digital user interface, but the issue is that the supply chain is not digitised, right from manufacturing schedules to inventory management and parts availability. How do we bring the Kashmiri Gate grey market retailer into the formal value system is a key question. So, we have a long way to go before a digital marketplace can meet customer expectations. What will surely help is greater levels of transparency and data exchange.’

If Danylenko hinted at the need for aftermarket stakeholders to collaborate, TecAlliance’s Deshpande amplified upon this thought. ‘As an industry we need to collaborate more to bring forward all stakeholders, be they manufacturers or service providers. Tech Alliance is a global partner for anything to do with aftermarket data and we are trying to promote standardized data through our catalogues. As industry, we need to break away from data silos. We have seen that over the last couple of years many of our partners are investing in cloud-based platforms or ERPs that can address demand forecasting, inventory management and customer outreach. ‘

Speed-A-Way’s Balasubramaniyam, addressed the audience from a unique perspective, ‘We are a nearly 75-year-old company, representing both vehicle OEMs and component manufacturers. We are able to combine traditional expertise with digitisation across functions like sales, channel management, real-time data analysis, payment processes as well as learning and development activities. We have also invested in virtual reality tools to help customers and channel partners choose components and services from the comfort of their homes and offices. Having said that, we are clear that digitisation must be common sense. Response time is critical. Part mismatches are high in digital transactions. So, we must be able to combine the offline and the online seamlessly, without being paralysed by too much analysis.’

The consensus of the panel was the digitisation needs to constantly evolve in sync with ground realities and that, it cannot be a short-term journey.

Electrification of Vehicles: Implications for the Aftermarket

The second panel consisted of Rama Shankar Pandey, CEO, Tata Green Batteries; Ramachandra Puttana, ZF’s Head of Aftermarket Business, Region India; Karn Nagpal, President, Rosmerta Group; Sathya AR, President, Ki Mobility Solutions; and Vivek Sharma, Founder and CEO, Fixcraft.in. The moderator was Vikas Yadav, Assistant Vice President, Techsci Research.

Tata Green Batteries’ Pandey asserted that, ‘e-mobility is a reality. But it has to be looked at from many dimensions, be it the spontaneous adoption of e-rickshaws or e-two-wheelers by e-commerce companies. Each one has their own needs. At the same time, we must be aware that as much as electrification, electronification of vehicles – more than 50% of vehicle content is electronics and software – has been a longer-term trend. Any roadside service station cannot get down to servicing vehicles. They need access to sophisticated tools, data from OEMs and most importantly training. So, there is a need for all players in the ecosystem – OEMs, tier 1 suppliers, independent service centres, customers and training centres – to collaborate.’

ZF India’ Ramachandra Puttanna couldn’t agree more, ‘We have created a new EV vertical over the last couple of years and it already contributes 9% of our revenues. This is because we work with the entire spectrum of OEMs and vehicles. While e-vehicles may have fewer moving parts, there is greater complexity and more value per part. So, we need a systems approach. Telematics will help track vehicle performance and driver behaviour. Battery management is another area where continuous monitoring must be linked with service networks. Over a period of time, we are likely to see the emergence of decentralised and large-scale battery swapping, disposal and recycling setups. We have gathered huge amounts of data across these fronts, which we are happy to share in the public domain and deploy the same for training all stakeholders.’

Ki Mobility’s Sathya observed, ‘Today, we have just about 8,00,000 electric two wheelers being sold as against 2 million internal combustion engine two-wheelers. So rather than look at e-mobility as a threat to our aftermarket business, we prefer to approach it as another important source of value addition. E-vehicles are generally put out by non-traditional OEMs, who operate with a start-up mindset, so they are more open to sharing data and collaborating. We would like to see this trend being accelerated with ICE vehicle manufacturers too.’

Fixcraft.in’s Vivek Sharma reasoned, ‘While there has been so much momentum in terms of online sales of vehicles and parts by e-commerce companies, we haven’t witnessed the same traction when it comes to independent service providers. That is where we stepped in five years ago. We are sure that OEMs realise that the greater the number of neutral service stations, the greater the uptime for their vehicles and therefore, better the vehicle sales. At the same time, we would urge for a greater role for insurance companies in specifying which parts may be used as open market substitutes to OEM parts to provide greater choices to customers. Alongside, we need greater visibility on how user data is being used in the pursuit of service. Data privacy in India is a joke.’

Rosmerta’s Karn Nagpal shared, ‘We contribute to the electrification in India in a few ways. Software-driven vehicles have to be connected whether it be for the aftermarket or for OEMs. Our platform connects more than three million vehicles today. Range anxiety is a concern for EV users. But a bigger concern is where can they get the best and most reliable service. Therefore, we have trained and provided diagnostic tools to a network of 400 aftermarket workshops who can service not just EVs but also ICE vehicles.’