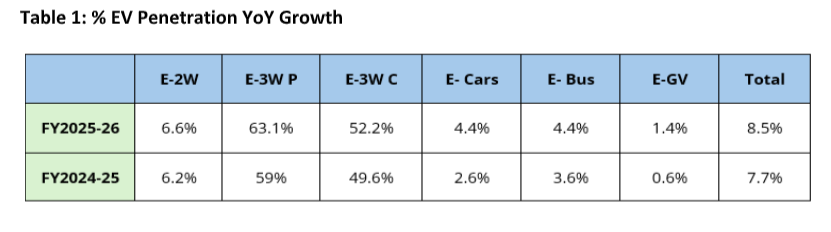

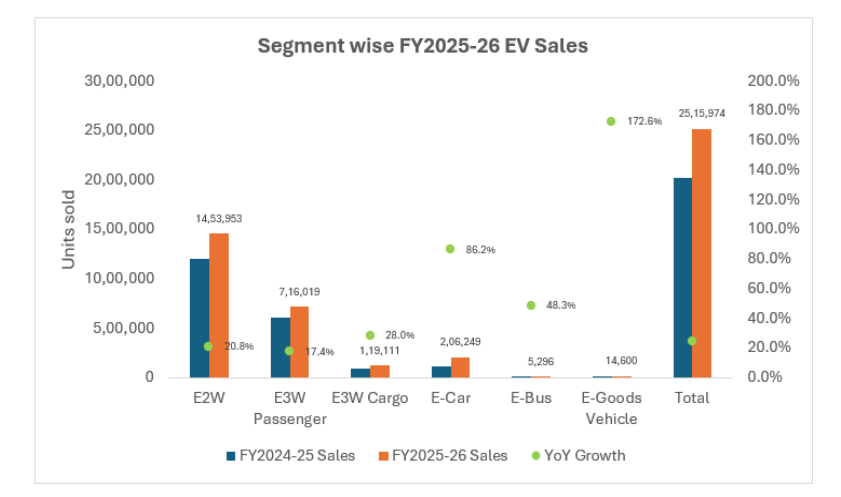

India’s electric vehicle (EV) market delivered another strong year in FY2025–26, with total registrations surpassing 25 lakh units – a 24% year-on-year increase. EV penetration reached approximately 8.5% of total registrations, up from 7.7% in the previous financial year. While this reflects a steady strengthening of EV adoption, the market still remains short of the government’s long-term target of 30% penetration by 2030.

Despite the price-sensitive nature of the market, growth drivers varied significantly across segments:

• Electric two-wheelers (E-2W): Continued as the largest contributor, accounting for nearly 58% of total EV sales.

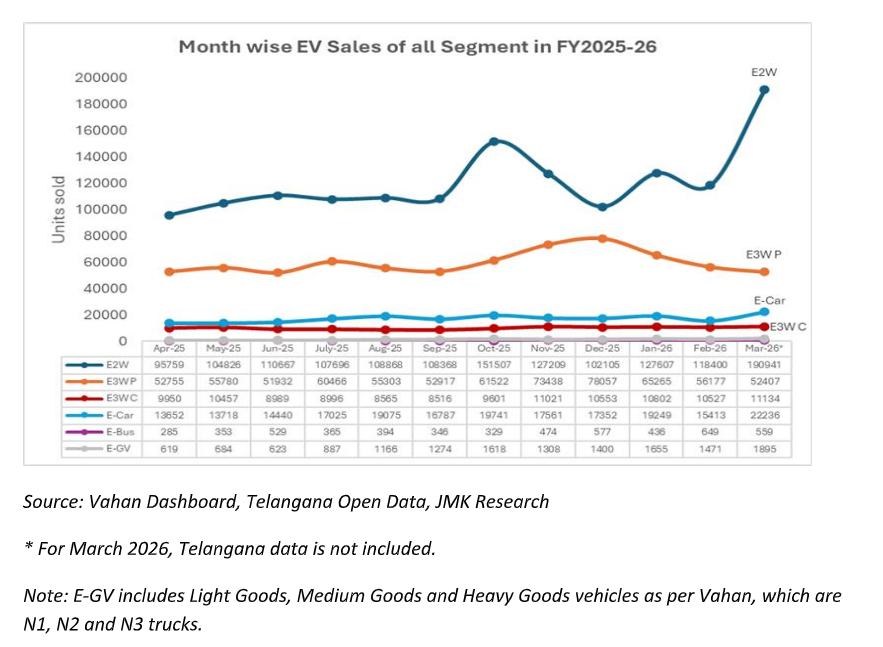

• Electric three-wheelers – passenger (E-3W P): The passenger segment peaked in December 2025 at 78,057 units, with the mandatory registration of e-rickshaws in West Bengal emerging as a key driver. However, sales moderated post-December 2025 as PM E-DRIVE incentives for the L5 category were exhausted.

• Electric three-wheelers – cargo (E-3W C): In contrast to the passenger segment, the cargo category witnessed steady growth, driven by Total Cost of Ownership (TCO) advantages for last-mile delivery fleets.

• Passenger vehicles (E-cars): Emerged as the fastest-growing segment, registering an impressive 86% year-on-year increase. Notably, this growth occurred independent of PM E-DRIVE support, as electric cars are excluded from the scheme’s purchase incentives – indicating strong organic demand.

• Electric goods vehicles (E-GV): Comprising light, medium and heavy goods vehicles, this segment recorded a significant 172% year-on-year growth, with adoption reaching 1.4% (up from 0.6% in FY2024–25). This surge was driven by the first-time inclusion of e-trucks (medium and heavy goods vehicles) under PM E-DRIVE incentives, increased uptake of light goods vehicles for last-mile logistics, and large-scale fleet electrification by e-commerce players aligned with corporate ESG goals.

Key Market Trends in FY2025–26

• Legacy OEMs gain share in electric two-wheelers: Traditional players such as TVS Motor, Bajaj Auto and Hero MotoCorp accounted for 61% of the E-2W market. Their success was underpinned by extensive dealer networks, robust after-sales ecosystems, improved product quality, and strong brand equity.

• Passenger EV market becomes more competitive: Tata Motors, while retaining leadership in the E-car segment, saw its market share decline sharply from approximately 57% in FY2024–25 to around 39% in FY2025–26. This was primarily due to intensified competition from JSW MG Motor, Mahindra and Hyundai, which expanded their presence through new product launches and sharper positioning.

The entry of VinFast and Maruti Suzuki in H2 FY2025–26 further intensified competition, particularly in the ₹12–25 lakh price band – a critical segment driving urban SUV demand. Concurrently, India’s charging ecosystem continued to scale, with public charging stations crossing 27,000 by March 2026, enhancing the practicality of electric SUVs for both urban and intercity use.

• March 2026 emerges as a record month: March 2026 recorded an all-time high of 2.8 lakh registrations. This surge was driven by a combination of year-end promotional pricing, anticipated price hikes, and heightened procurement activity from commercial fleet operators. Additionally, buyers accelerated purchases to avail benefits under the PM E-DRIVE scheme ahead of incentive deadlines for E-2Ws and E-3Ws.

Outlook for FY2026–27

The strong close to FY2025–26 establishes a solid foundation for the coming year. The Indian EV market is well-positioned to achieve a penetration rate of 9.5% to 10% in FY2026–27. This trajectory appears achievable, supported by the extension of PM E-DRIVE deadlines for electric two-wheelers and three-wheelers (L3 category) until July 31, 2026, and March 31, 2028, respectively.

Sustained momentum toward double-digit penetration will, however, hinge on continued expansion of charging infrastructure, deeper localisation across the value chain, improved financing accessibility, and a steady pipeline of new product introductions.